The time may be ripe to rethink the consolidation model for financial statements and the definition of control, in connection with, among other things, publicly‑held subsidiaries. The main reason for this is the increase over the years of the legal and regulatory “proper corporate governance” requirements for publicly‑held companies, which poses a challenge to the conceptual basis of existence of “control” of a “parent” over every single asset of its publicly‑held subsidiaries. A model that contracts the definition of control on the basis of combination of certain criteria, such as, easy and simple transfer of money between the parent and the subsidiary, an operational relationship between them and a lack of an unusual separation in the corporate governance, could serve to improve the relevance of the financial statements from the standpoint of investors and prevent the range of distortions deriving from them at the present time. This post includes examples from the Israeli market.

Even though the model for consolidation of financial statements is a basic and foundational accounting concept that has enjoyed a broad consensus in the world’s leading accounting standards (IFRS and U.S. GAAP) for many years – it seems that the number of reasons for its suitability and necessity appearing in the said accounting standards (as well as in the academic literature) is relatively sparse. The consolidation model is based on the existence of control of the reporting entity over the investee – which as a result is defined as a subsidiary. The concept underpinning the model is the existence of economic control, as opposed to formal/legal control, over each and every one of the subsidiary’s assets, and as a result also constitutes an economic (and not a legal) obligation for all of its liabilities. Along with the consolidated statement of financial position, the consolidated financial statements also present the results of the group companies – such that the statement of profit or loss and statement of cash flows are also presented on a consolidated basis.

In the spirit of accounting theory, the rationale for the model for consolidation of financial statements is giving preference to economic substance over legal form. This can be easily illustrated by the basic case of a wholly‑owned subsidiary. Taking a simple case of a company whose entire business consists of holding a wholly‑owned subsidiary that owns a lot (a land parcel) and that has no debt, the financial statements will be more relevant if a consolidated statement of financial position is presented that includes an investment in a lot rather than presentation of a separate statement of financial position that presents an investment in a subsidiary. Similarly, where part of the activities of a certain group is carried out, as a formal matter, through one or more subsidiaries and not solely by the parent, for example, a group that is engaged in construction of units for sale, where a wholly‑owned subsidiary is the contractor of the parent, it would be appropriate to present the activities of the entire group as a single unit (entity). Absent a requirement to consolidate, it would indeed be possible to make simple manipulations in order to change the business position presented to the users of the financial statements without changing the economic substance. A good illustration of this point is the Enron accounting scandal, where use was made of off‑balance sheet entities in order to “dress‑up” the actual financial position and later on the group experienced a shocking crash in the beginning of the 21st century.

The tension between the idea of control and corporate governance

The conceptual difficulty starts when a subsidiary that is not wholly‑owned is involved. As long as the subsidiary is a private company, the rationale for the consolidation can be understood – even where it is not wholly‑owned. The reason for this is that, generally, the parent’s control of the subsidiary’s operations exists, including with respect to every significant decision. That is, the non‑controlling interests are essentially a passive partner.

The above case can be quite easily compared to a situation where instead of holding a subsidiary, the parent itself issues preferred shares that are classified as equity, but with no voting rights, where the holders of those shares have preferred legal status in a case of liquidation with respect to an identified group of net assets (“silo”). From an economic standpoint, these preferred shares, which do not belong to the holders of the ordinary shares, are essentially similar to non‑controlling interests, which are clearly an equity item in the consolidated statement of financial position that does not belong to the shareholders of the parent.

The real problem with the existing consolidation model arises where a publicly‑held subsidiary is involved. This problem has become more pronounced in the past decades due to the stricter corporate governance requirements, mainly separation between the shareholders and the subsidiary’s Board of Directors, which is required to act in the company’s overall best interest, along with the sharp increase in the safeguards granted to the non‑controlling shareholders, such as regarding approval of transactions with the controlling shareholder and salaries paid to managers. Proper enforcement of the corporate and securities’ laws that leads to proper corporate governance in a publicly‑held subsidiary should lead to the control premium being about zero. In such cases, the majority shareholders are prevented from intervening in the subsidiary’s activities, except for appointment of qualified directors – however, these directors are required to make decisions solely for the benefit of the subsidiary. For example, in the past the Supervisor of the Banks in Israel did not allow the controlling shareholder in Bank Hapoalim, Ms. Shari Arison, to participate in the meetings of the Board of Directors, to coordinate positions or even to speak with the directors. The almost total erosion of the essence of control ultimately caused Ms. Arison to relinquish the control and at the present time the owners of most of the large banks in Israel are dispersed, without there being any controlling shareholder at all.

An expression of proper corporate governance in publicly‑held companies can be observed, for example, in the United States, where the incentive for holding control shares is relatively low. In Israel, this can easily be seen in regulated financial entities, such as banks and insurance companies, where the controlling shareholder’s ability to intervene is very limited. In addition, the average control premium regarding all the publicly‑held companies in Israel has also been significantly eroded in the last decade.

The problem, as I see it, lies in the definition of “control”, or at least in the manner it is customarily applied, which relates to the “power” to make decisions regarding the relevant activities – operational and financial. Thus, for example, despite the fact that IFRS 10, the international financial reporting standard addressing consolidation of financial statements, whose main issue is the determination of control, is relatively new, it arguably does not prevent the existence of control in a case where the subsidiary is publicly held and it has strict corporate governance. In these cases, determination that the majority shareholder could influence decisions made by the subsidiary’s Board of Directors, and thus he/it effectively has control over every asset, appears to be quite problematic. There is built‑in tension between the concept of control and the appropriateness of the corporate governance, such that the more appropriate the corporate governance is, the weaker the control is up to the point of total elimination.

The proposed model

In light of that stated above, it is proposed to consider adoption of an alternative reporting model that will limit the definition of control for purposes of consolidation of financial statements, on the basis of a mix of the following criteria:

- “Ability to transfer money” – simple and easy, with no significant limitations, between the parent and the consolidated subsidiaries.

- Significant operational relationship among the group companies – such as numerous intercompany transactions, vertical production and supply chain, structures for tax savings or cooperation with local partners in other countries.

- Absence of separation in the corporate governance or the corporate structure – such as where there is no significant separate regulatory supervision, a significant partner having special rights or significant geographic separation.

The proposed change is expected to create a gap between the definition of control for accounting purposes and the broader definition thereof for purposes of the securities laws. This gap is appropriate since the purpose of the definition of control in the securities laws is protection of the non‑controlling interests and not control in the sense of consolidation of every asset and liability as if they belonged to the parent. That is, it is very important to make a distinction between the different uses made of the definition of control, even if such definition is similar in the different areas.

It is noted that occasionally the problem with the existence of control for reporting purposes is also present where a private subsidiary is involved, where there is a specific regulator that seeks to tighten the corporate governance requirements. For example, in Israel, for historical reasons, the large insurance companies are private companies and are wholly owned by publicly‑held holding companies. In light of the strict requirements of the specific regulator – the Supervisor of the Capital Market – there is no possibility for the publicly‑held parent to intervene in the decisions of the insurance subsidiary. These matters have become more acute in recent years in the case of Migdal Insurance Company, where the Supervisor of the Capital Market did not allow Mr. Shlomo Eliahu, the controlling shareholder, to intervene in the management of the private insurance company.

A similar situation exists where a strategic partner enters into a private subsidiary, who receives by means of shareholders’ agreements preference rights that sometimes include limitations on withdrawal of monies and distribution of dividends from the subsidiary to the parent. In such cases, the existing criteria in the definition of control in the accounting standards would appear to be met, even though logic would dictate that such companies should not be consolidated in light of the proposed model.

It is important to emphasize that beyond the composition of financial statements, limitation of the definition of control for purposes of consolidation of financial statements would also prevent distortions that presently occur due to the relative frequency of entries into and exits from the control definition. These “movements” in the control status trigger, according to the theoretical realisation concept, recording accounting income, when frequently no real change in status has actually taken place.

Analysis of financial statements of holding companies

Without addressing its business justification, the holding model whereby one publicly-held company holds another publicly-held company is not widespread in many countries worldwide for a variety of reasons, including regulatory and tax reasons. However, to the extent that it does exist, consolidation of the financial statements of a publicly‑held subsidiary could confuse and even mislead the investors in the parent.

For example, a working capital ratio that indicates solid liquidity could be misleading since the cash balance is not always in control and it is not necessarily true that cash balances of the subsidiaries and second‑tier (lower‑tier) subsidiaries may be distributed as dividends along the holding chain. One of the most vivid stories regarding this matter in Israel took place in the mid 1980’s where Danot Investment Company Ltd., which had control over Bank Benleumi, became insolvent despite the positive consolidated shareholders’ equity, due to the inability to utilise resources of Bank Benleumi.

A further example relates to one of the most painful debt arrangements in Israel, which took place about ten years ago, relating to the Africa Israel Investments group, which despite the fact that it had a liquidity problem, it presented a large cash balance in its financial statements (stemming from the subsidiaries), which could apparently be construed as it having the ability to make the payments required to service its debentures. The financial leverage can also be misleading – for example where the holding company at the top of the pyramid is in the midst of difficulties, but the subsidiaries are in a relatively good position, the consolidated financial statements will show an erroneous picture.

It is noted that the disclosure requirements of IFRS 12, with reference to the significant subsidiaries and non‑controlling interests, do not necessarily have the ability to prevent the above‑mentioned reporting distortion, even if the complication deriving from such an analysis by means of the notes is ignored. Moreover, full adjustment of consolidated figures might not be practical when performed by investors that do not have sufficient accounting expertise, and it may also not necessarily be capable of being fully executed.

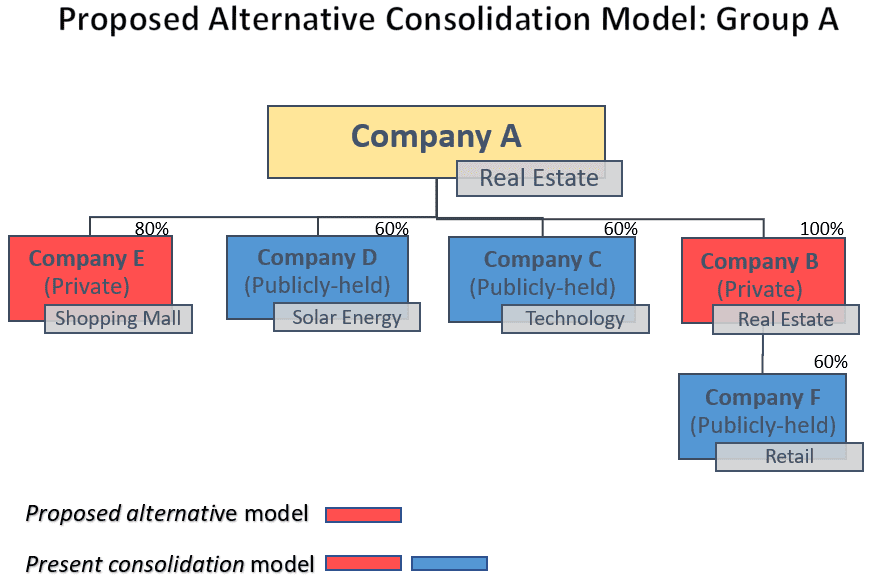

The gap between the existing consolidation model and an alternative consolidation model known as the “expanded separate” model, which constitutes at least a partial solution to the control issue in publicly‑held subsidiaries, can be illustrated with the following example. It is assumed that Company A is a real estate company that owns rental properties and has four investees over which it has “control”, as follows:

Pursuant to the existing accounting standards and the manner in which they are applied in the group’s consolidated financial statements, all of the five above‑mentioned companies will be consolidated (including Company F). Conversely, based on the principle that the financial statements of publicly-held companies will not be consolidated, the result is that the primary financial statements of Company A will include a consolidation of only Company B and Company E, while the investments in Company C, Company D and Company F will be included in a single number (“expanded separate”). In this situation, the main figures in the primary financial statements – such as revenue, operating profit and assets will include only the data relating to the real‑estate activities.

Following are the companies that will be consolidated in the financial statements of Company A:

It should be borne in mind that the note on operating segments that is intended to provide relevant information on a segment basis, is not a comprehensive solution to every reporting problem. That is, where the reporting base is overly broad, the relevance of the information is eroded, even where operating segments are disclosed in a note. Moreover, the higher its resolution, the more effective the information is to investors, provided, of course, that it is properly applied.

Consistent with the standpoint of the investors, the perspective of the boards of directors of the consolidated financial statements can also be observed. For example, some of the holding companies in Israel in the real estate area – such as Azrieli and Alony Hetz, analyze the periodic results presented to the directors based on the “expanded separate” method – which essentially presents consolidated financial statements without consolidation of publicly-held subsidiaries (which are accounted for as one asset – “investment in shares”).

In any case, it is important to note that even if the primary financial statements are prepared on the basis of consolidation of only private subsidiaries (“expanded separate”), there is still a significant gap between the composition of such financial statements and separate financial statements, which present only the assets and liabilities of the legal entity.

And for an encore – inferiority of the equity method of accounting

When carrying on a discussion of discontinuing the consolidation of financial statements of publicly-held companies, a good opportunity also is presented to reconsider the efficacy of application of the equity method of accounting, which is replete with accounting problems. The equity method of accounting for investments in associates is in any event quite weak where investments in shares of companies with no significant influence are measured at fair value. Where a publicly-held company is involved, a fair value estimate of the investment at Level 1 (active market) is necessarily available. For example, the Israeli holding company Discount Investments, which has holdings in a number of publicly-held subsidiaries, reports quarterly, at its own initiative, as part of the Directors’ Report (which is not part of the financial statements), its “net asset value” (NAV) on the basis of the market value of the investments in the listed subsidiaries and associates. This means that the holding company deems this information to be relevant to its investors. It should be borne in mind that, as opposed to private equity funds and other similar funds that are generally non‑public, the publicly-held holding companies usually do not meet the definition of an “investment entity”, which at the present time leads to a different and special reporting model, whereby subsidiaries are not consolidated, while, on the other hand, measurement of the investments therein is made on the basis of fair value through profit or loss.

It is noted that since already about a decade ago, the possibility exists under U.S. GAAP as part of the “fair value option” to choose to measure investment in associates at fair value through profit or loss, instead of applying the equity method of accounting. As a result, it is appropriate to examine whether, in the first stage, measurement of investments in publicly-held investees at fair value on the basis of their market price should be permitted, and even encouraged, which would serve to increase the relevance of the financial statements of the holding company – at no significant cost. Such a change, which should be accompanied by the possibility to designate all the investments in publicly-held investees as at fair value through profit or loss, could also lead in the future to doing away with the equity method of accounting for private associates.

(*) Written by Shlomi Shuv